Nvidia Q1 2026 earnings revenue Vera chip data center results confirmed another quarter of performance that exceeded analyst expectations, with the world's most valuable company reporting first-quarter revenue of $81.62 billion against the average analyst estimate of $78.86 billion, forecasting second-quarter revenue of $91 billion plus or minus 2 percent well above Wall Street estimates of $86.84 billion, and announcing an $80 billion share repurchase programme alongside a dividend increase to 25 cents per share from 1 cent, while simultaneously unveiling the Vera central processor architecture as a new business that CEO Jensen Huang said targets a $200 billion market and is expected to generate $20 billion in revenue by the end of the fiscal year. Despite the beat on revenue and the above-consensus Q2 forecast, shares fell 1.6 percent in extended trading, a market reaction that eMarketer analyst Jacob Bourne articulated precisely: Nvidia delivered another beat, but at this point that is essentially priced in as it keeps beating quarter after quarter, with the lingering question being whether it can convince investors the AI buildout has durability into 2027 and 2028, especially as the narrative shifts toward inference workloads and competing silicon from Google, Amazon, AMD, and Intel.

Data center revenue in the quarter came in at $75.2 billion, ahead of the average analyst estimate of $72.8 billion, with Huang pointing to a new sub-segment of AI-specific cloud customers whose sales were roughly equal to the large cloud players but grew faster quarter-over-quarter as evidence that Nvidia's customer base is broadening beyond the hyperscale concentration that has characterised its revenue mix. Huang told analysts on the conference call that he believes Nvidia should be growing faster than hyperscale capital expenditure, pointing to AI-specific cloud firms as the growth engine that will sustain the company's expansion beyond the pace of the Alphabet, Amazon, and Microsoft spending programmes that are expected to exceed $700 billion on AI infrastructure this year, a sharp jump from approximately $400 billion in 2025. Adjusted earnings per share of $1.87 exceeded market estimates of $1.76, with Nvidia also disclosing $30 billion worth of cloud computing agreements up sequentially from $27 billion, arrangements that analyst Jay Goldberg of Seaport described as backstops in which Nvidia agrees to pay cloud computing companies for excess capacity from systems running Nvidia hardware.

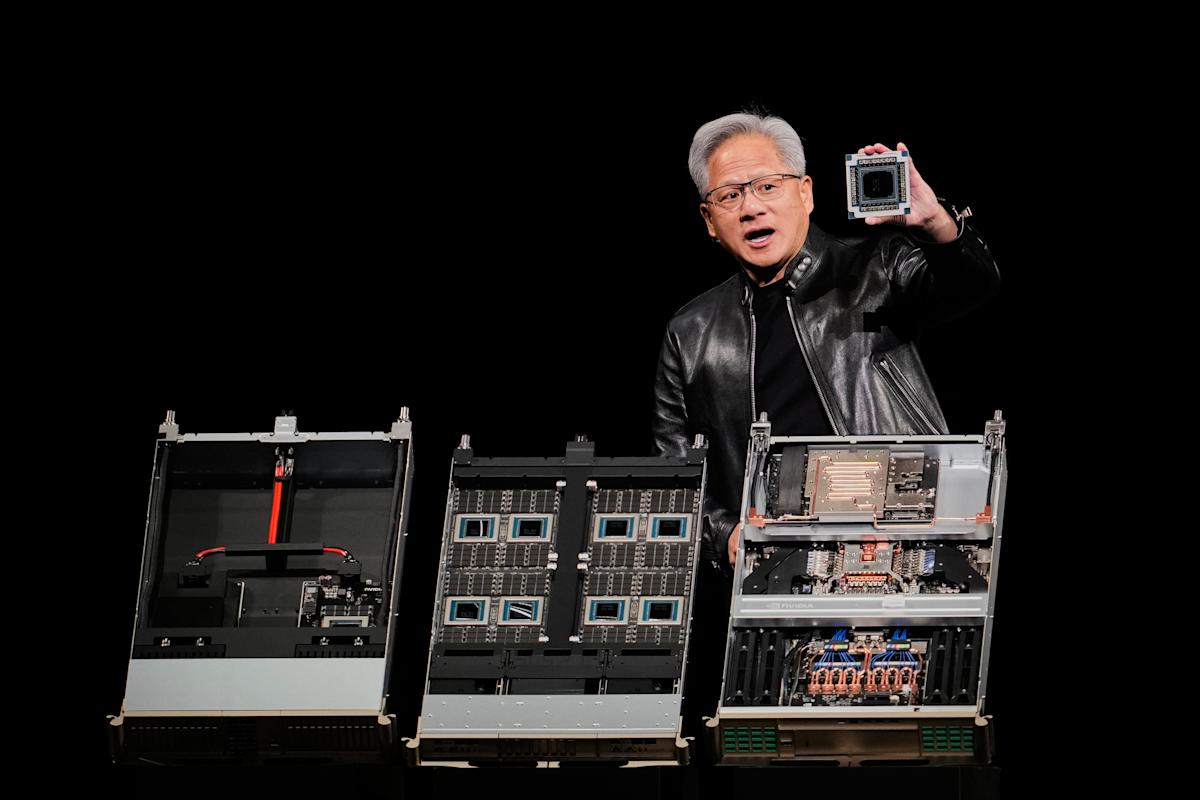

The Vera central processor that Huang introduced as the company's access point to a new $200 billion market was explicitly identified as not included in Nvidia's earlier $1 trillion estimate for Blackwell and Rubin AI chip sales between 2025 and 2027, meaning the Vera revenue represents additive opportunity rather than a reclassification of previously forecast sales. Huang described Vera as expected to become the second-largest sales contributor beyond the trillion-dollar Blackwell and Rubin franchise, a forecast whose magnitude would make it among the largest single product introductions in semiconductor history if realised, and noted that all of the company's customers were quite excited about the architecture. The Vera chip built on technology from Groq, the inference-specialising startup whose technology Nvidia incorporated in March, represents Nvidia's strategic response to the inference market opportunity that AMD, Intel, and the hyperscalers' own custom silicon efforts are targeting as the AI workload mix evolves from the training-dominated early buildout phase toward the inference-heavy deployment phase that scale AI adoption represents.

How Nvidia Built Its AI Dominance and What Is Now Challenging It

Nvidia's Blackwell GPU architecture, which has been the primary driver of the extraordinary revenue acceleration that took the company from a gaming and professional visualization chipmaker to the world's most valuable company across the AI boom period beginning in 2023, represents the technological foundation on which the trillion-dollar sales forecast through 2027 is built. The Blackwell architecture's combination of raw processing performance for AI training workloads, the CUDA software ecosystem that gives Nvidia chips a decisive advantage in programmer adoption and library compatibility, and the NVLink interconnect technology that allows multiple GPUs to work together with high bandwidth create a competitive position that AMD and Intel have been working to replicate without achieving the same level of market penetration. Nvidia's data center revenue trajectory from single-digit billions per quarter in 2022 to the $75.2 billion reported for Q1 2026 documents a business expansion of a pace and magnitude that the semiconductor industry had not previously experienced.

The trillion-dollar Blackwell and Rubin sales forecast, which Huang confirmed the Vera $20 billion does not reduce or replace, reflects the hyperscaler capital expenditure commitments that Alphabet, Amazon, Microsoft, and Meta have been making for AI infrastructure buildout that extends over multiple years of construction, equipment installation, and system integration. U.S. tech giants are expected to spend more than $700 billion on AI infrastructure in 2026 alone, with the majority of that spending flowing through Nvidia's data center GPU business because of the CUDA ecosystem lock-in and the performance advantages of Nvidia hardware for training the largest AI models. This spending trajectory, if maintained through 2027 and 2028, provides the revenue visibility that makes the trillion-dollar forecast credible, but Bourne's lingering question about durability is precisely whether the hyperscaler spending programmes will sustain at current growth rates or whether demand saturation, alternative silicon development, or economic disruption will slow the buildout before Nvidia's forecast is realised.

The supply constraints that Huang acknowledged would persist through the entire life of the Vera Rubin platform, the combined chip system launching later this year, reflect the memory chip crunch and manufacturing capacity limitations that constrain Nvidia's ability to meet demand even at current extraordinary revenue levels. Nvidia's supply rose to $119 billion in the fiscal first quarter from $95.2 billion in the previous quarter, documenting the scale of the inventory build the company is making to ensure supply chain resilience during the global memory chip shortage. The supply growth is an investment in future revenue capacity rather than a reflection of current demand weakness, because Nvidia's order books reflect excess demand relative to production capacity rather than the reverse, and the company's priority is ensuring that supply chain snags do not prevent it from capturing the revenue that customer demand makes available.

The Inference Market and Why It Is Creating Competitive Vulnerability

The shift in AI workload composition from training-dominated to inference-dominated as AI models move from development to deployment represents the most significant structural change in the AI chip market that Nvidia's competitive position must navigate, because the inference market's performance requirements and economics differ from training in ways that create opportunities for alternative chip architectures to compete more effectively than they have in the training segment. Training large AI models requires the sustained peak GPU performance and memory bandwidth that Nvidia's flagship chips provide and that AMD and Intel have struggled to match, but inference, which involves running already-trained models to generate responses and outputs for end users, has different computational requirements that are more amenable to the efficient, purpose-built silicon that Google's TPUs, Amazon's Trainium and Inferentia, and the custom chips that other hyperscalers are developing can potentially serve more cost-effectively than Nvidia's general-purpose GPUs.

AMD and Intel have both identified the inference CPU market as their primary competitive opportunity against Nvidia, with both companies articulating a large revenue opportunity from selling central processors that handle inference workloads more efficiently than Nvidia's GPU-centric approach. Intel's forecast last week of second-quarter revenue exceeding Wall Street expectations had already demonstrated the competitive momentum that alternative chip providers are building in the AI infrastructure market, and the inference market opportunity they are targeting provides a structural avenue for AMD and Intel to capture market share that was unavailable to them in the training-dominated early AI buildout. Nvidia's introduction of Vera, built on Groq's inference-specialised technology, is its direct response to this competitive threat, creating a CPU product specifically optimised for the inference workloads that its data center GPU customers are scaling up as their AI deployments move from training to serving users.

The Vera Opportunity, the $80 Billion Buyback, and What Investors Are Watching

Huang's identification of a $200 billion addressable market for Vera central processors, with $20 billion in expected revenue by the end of the current fiscal year, is the most strategically significant disclosure of the earnings call because it documents Nvidia's determination to participate in the inference market segment that its GPU-focused business model has not historically addressed with purpose-built architecture. A $200 billion CPU market opportunity would represent a major expansion of Nvidia's total addressable market beyond the GPU and accelerated computing segments where its current dominance is concentrated, and the $20 billion fiscal year revenue forecast signals that the opportunity is not aspirational but is backed by customer commitments sufficient to support a near-term production and sales plan. The Groq technology that underpins Vera represents Nvidia's recognition that the most competitive inference silicon requires architectural innovation specifically targeted at inference rather than adaptation of GPU architectures designed for training.

Huang's acknowledgment that Nvidia will be supply-constrained through the entire life of the Vera Rubin platform is simultaneously a positive commercial signal, confirming that demand exceeds available supply, and a business risk, because supply constraints limit revenue growth even when demand would support faster expansion. Managing supply chain complexity across multiple new product introductions, including Vera and the Rubin platform, while also maintaining supply for the existing Blackwell product cycle creates the operational challenge that the $119 billion supply build documented in Q1 is designed to address. Nvidia's financial resources and supplier relationships give it the capacity to make these supply investments at a scale that smaller competitors cannot match, but the technical complexity of advanced semiconductor manufacturing means that supply chain risks remain even for the best-resourced companies.

The $80 billion share repurchase programme announced alongside the earnings results is the capital return signal that confirms Nvidia's management assessment that even at the current extraordinary revenue and profit levels, the company generates sufficient cash flow to fund both its operational investments and substantial return of capital to shareholders. A company expecting supply constraints through the life of its current product cycle and investing in the supply chain to address those constraints while simultaneously announcing $80 billion in buybacks is demonstrating confidence that its cash generation will remain more than adequate to fund all of these commitments simultaneously. For investors questioning the AI buildout's durability, the buyback's scale is management's most direct expression of confidence in the revenue trajectory that makes such capital return sustainable.