Vestas Q1 2026 profit offshore wind turbine production acceleration delivered the Danish wind turbine maker's highest first-quarter profitability since 2018, with operating profit before special items rising to 127 million euros from just 14 million euros a year earlier, dramatically exceeding the mean analyst forecast of 71 million euros in the analyst poll shared by Vestas and confirming that the company's multi-year struggle to turn a record backlog into meaningful margins is beginning to produce the financial results that investors and management have been working toward. CEO Henrik Andersen said the result demonstrated the highest first-quarter profitability since 2018, framing the outcome against a challenging recent history of supply chain disruptions, cost inflation, and offshore production ramp-up costs that had suppressed margins well below the levels that Vestas's order backlog would in a normalised operating environment generate. The operating margin widened to 3.2 percent from just 0.4 percent a year earlier, a near-eightfold improvement in margin percentage that reflects both the operational progress of the offshore production scale-up and the cost discipline that management has been applying across the business.

Vestas maintained its full-year guidance for an operating profit margin before special items of 6 to 8 percent on sales of between 20 billion and 22 billion euros, the same guidance it provided in February, signalling that the stronger-than-expected first quarter has not yet created sufficient visibility to justify raising the annual target even as it validates the trajectory toward the guided range. In 2025, Vestas achieved a margin of 5.7 percent on sales of 18.8 billion euros, providing the baseline from which the 2026 guidance represents a meaningful improvement that would confirm the company's recovery from the trough conditions of recent years. First-quarter sales rose 14 percent to 3.97 billion euros, slightly above expectations, driven specifically by offshore turbine sales as the production ramp-up that has been the central operational challenge and the central opportunity for Vestas over the past two years gained meaningful commercial pace.

Andersen's statement that the current geopolitical uncertainty and energy crisis underline the need for affordable, secure, and sustainable energy reflects the specific macro context in which Vestas is reporting its results, a world in which the Iran war's disruption of fossil fuel energy supplies has made the energy security case for wind power more urgent and more politically compelling than it has been at any point in the past decade. The global energy crisis created by the Strait of Hormuz closure has elevated the political salience of renewable energy investment in ways that provide tailwinds for Vestas's order pipeline even as the same geopolitical environment creates tariff and trade policy uncertainties that complicate the supply chain economics of actually delivering against that pipeline. The company's record backlog and the 4.50 gigawatt order intake for the first quarter, including especially strong offshore activity, document the commercial reality that demand for wind turbines is being driven by exactly the energy security imperative that Andersen described.

How Vestas Built Its Global Wind Leadership and the Challenges That Tested It

Vestas has been one of the defining companies of the global wind energy industry since its founding in Denmark in the 1940s and its pivot toward wind turbine manufacturing in the 1970s, a period when the oil shocks of that decade created the first serious political and commercial interest in renewable energy alternatives to fossil fuels. The company grew from a Danish manufacturing business into the world's largest wind turbine manufacturer over several decades of technological development, market expansion, and the scaling of wind energy from a niche alternative technology into one of the lowest-cost electricity generation sources in the world. Vestas's turbines operate in more than 80 countries, and the company has installed a total turbine fleet whose cumulative generating capacity represents a meaningful contribution to global renewable electricity supply across multiple continents and market structures.

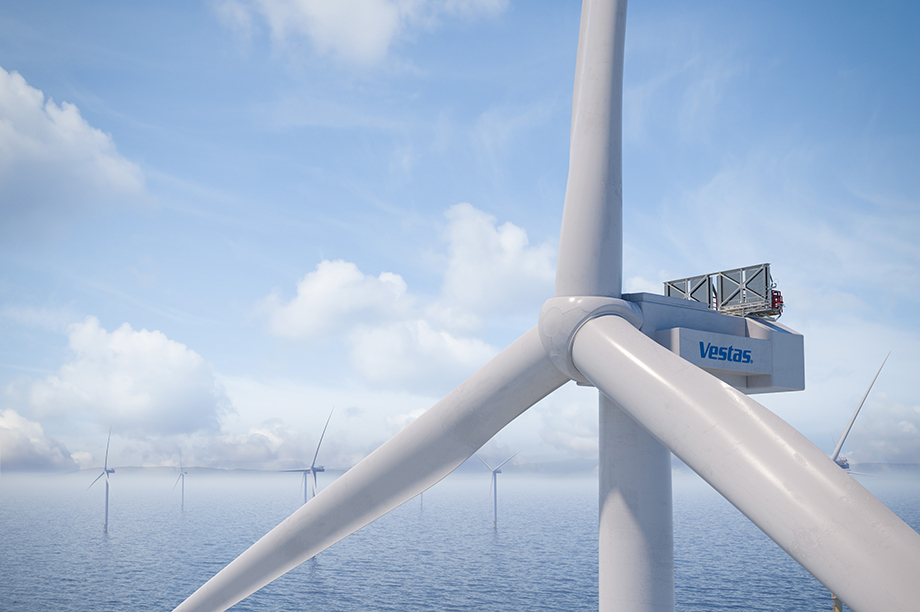

The offshore wind segment that is driving Vestas's current recovery represents the industry's next major growth frontier, moving wind energy from its established position in onshore markets into the deeper water marine environments where wind resources are stronger and more consistent than on land and where the scale of individual installations can be larger than anything achievable in onshore settings. Offshore wind development requires a fundamentally different industrial and logistics infrastructure than onshore wind, including specialised installation vessels, offshore-rated electrical systems, foundations engineered for marine conditions, and supply chains capable of delivering components of extraordinary size to remote maritime locations. The ramp-up costs and operational complexity of building this offshore infrastructure have been the primary source of the margin pressure that Vestas has experienced in recent years, as the company invested in offshore production capacity ahead of the revenue stream that capacity would eventually generate.

Vestas's record backlog, accumulated during a period of strong order intake but constrained production capacity, represents the deferred revenue that the company is now beginning to convert into actual deliveries and recognised revenue as its offshore production capabilities reach commercial scale. A backlog is simultaneously a measure of commercial success, confirming that customers want Vestas turbines, and a source of operational pressure, committing the company to deliveries at prices agreed when the backlog was booked that must be met with production costs that may have changed since the original contracts were signed. Vestas's ability to maintain its guided margin range as it works through the backlog depends on managing production costs, logistics costs, and installation complexity within the parameters that the original contract economics assumed, a challenge that supply chain disruptions and cost inflation have made significantly harder in recent years than the order-booking period might have projected.

Supply Chain Disruptions, Cost Inflation, and the Offshore Ramp-Up Challenge

The supply chain disruptions that Vestas acknowledges as a significant challenge in recent years reflect the specific vulnerabilities of large offshore wind turbine manufacturing, which depends on specialised components including large-diameter bearings, high-capacity gearboxes, permanent magnet generators, and composite blade materials that are produced by a limited number of specialist suppliers with long lead times and limited capacity to quickly expand output in response to demand increases. When supply chain disruptions affect these critical components, Vestas faces a binary choice between delaying deliveries to customers and absorbing the contractual penalties that delays trigger, or paying above-contract prices for alternative supply sources to maintain delivery schedules. Both choices damage margins, and the combination of supply disruptions and cost inflation in the post-pandemic period created exactly the environment where Vestas faced both simultaneously across multiple projects and markets.

The cost inflation component of Vestas's recent challenges reflects the broader inflationary environment that affected all industrial manufacturers through 2022 and 2023, but with specific intensity in the steel, copper, and composite materials that wind turbines consume in large quantities. Offshore wind turbines require more steel per megawatt of generating capacity than onshore turbines due to the structural demands of offshore foundations and tower designs, making them particularly sensitive to steel price inflation. The simultaneous increase in materials costs, energy costs for manufacturing, and logistics costs for the specialised shipping required to move large components to offshore installation sites created a perfect storm of cost pressure that compressed margins on fixed-price contracts signed before the inflation episode began.

The offshore ramp-up costs that Vestas specifically identifies as a challenge category reflect the learning curve and fixed cost absorption dynamics of scaling a new production system to commercial volumes. When Vestas invests in the dedicated manufacturing facilities, tooling, and workforce training required to produce offshore turbines at scale, those investments create fixed costs that are absorbed across the turbines produced in each period, meaning that the per-unit cost is highest when production volumes are lowest in the early ramp-up phase and declines as volumes increase and fixed costs are spread across more units. The improvement in first-quarter margins from 0.4 percent to 3.2 percent year-on-year is partly a reflection of this volume absorption dynamic, as offshore production volumes in the first quarter of 2026 were significantly higher than a year earlier, spreading fixed costs across more turbines and reducing the per-unit cost that determines margin.

The US Policy and Trade Tariff Uncertainty

Vestas's warning about uncertainty around geopolitical developments and trade tariffs reflects specific risks in the U.S. market, which has been one of the wind industry's most important growth markets but has become significantly more uncertain under the Trump administration's policy posture toward renewable energy and international trade. The Inflation Reduction Act's renewable energy tax credits, which drove a wave of U.S. wind energy investment following their enactment in 2022, have faced political uncertainty under the current administration's policy priorities, creating questions about the investment case for projects whose economics depend on those credits persisting through their project development and construction timelines. Trade tariffs on components used in wind turbine manufacturing, including steel, aluminium, and specialised mechanical components, add cost and supply chain complexity that affects Vestas's U.S. project economics.

The U.S. wind policy uncertainty is particularly consequential for offshore wind development, where project timelines extend over many years from initial planning through permitting, financing, construction, and commissioning, meaning that policy changes at any point in that extended timeline can fundamentally alter a project's economics. Several U.S. offshore wind projects have been cancelled or delayed in the current policy environment, reflecting developer assessments that the combination of policy uncertainty, permitting delays, and supply chain cost inflation make some projects economically unviable at the power purchase agreement prices that were agreed when the projects were contracted. Vestas's exposure to this U.S. offshore market uncertainty is real but is partially offset by the strength of European and Asia-Pacific offshore demand that is driving the strong order intake the company reported for the first quarter.

The trade tariff component of Vestas's uncertainty warning is directly connected to the broader trade policy environment that the Trump administration has created and that the Supreme Court has partially addressed through its ruling striking down the emergency tariffs. For a wind turbine manufacturer whose supply chains span multiple continents and whose product deliveries require importing components from European and Asian suppliers into installation sites in the United States, tariff costs on imported components can meaningfully change the economics of U.S. project delivery and affect the competitiveness of bids for new U.S. projects. Vestas's ability to pass tariff costs through to customers depends on contract structures and competitive dynamics that vary by project and market, making the tariff impact difficult to predict or fully hedge.

Record Backlog, Order Momentum, and the Path to Full-Year Guidance

The first-quarter order intake of 4.50 gigawatts, up from 3.14 gigawatts a year earlier, is the commercial validation that Vestas's backlog is being sustained and expanded even as the company works through existing orders, confirming that customer demand for Vestas turbines continues to generate new commitments at a pace that replenishes the pipeline rather than simply depleting it as deliveries are made. The order intake was driven by onshore orders across regions and especially strong offshore activity, reflecting the energy security imperative that the Iran war has intensified across multiple markets where governments are accelerating renewable energy deployment to reduce fossil fuel import dependence. The combination of ongoing onshore order strength and accelerating offshore order momentum provides the demand foundation that supports Vestas's 20 to 22 billion euro sales guidance range for the full year.

The especially strong offshore order activity in the first quarter is the most strategically significant element of the order intake data, because offshore wind represents the segment where Vestas's competitive position, technological capability, and production investment create the greatest differentiation from competitors and the greatest long-term margin opportunity. Offshore wind contracts typically involve larger per-project value, longer delivery timelines, and more complex service arrangements than onshore projects, creating the kind of high-value customer relationships that support the premium pricing and margin structures that Vestas needs to achieve its guided operating profit margin range. Growing offshore order intake alongside accelerating offshore production is the virtuous cycle that Vestas's recovery strategy depends on, and the first-quarter data confirms that cycle is operating in both dimensions simultaneously.

The 100 million euro share buyback that Vestas announced alongside the first-quarter results is a capital allocation signal that management is confident enough in the business's cash generation trajectory to return capital to shareholders rather than retaining it for operational or investment purposes. Share buybacks at companies emerging from difficult operational periods carry specific signalling value because they communicate management's assessment that the improvement in financial performance is durable rather than temporary, since buying back shares at current prices creates shareholder value only if the business continues to perform at or above the level implied by those prices. Vestas's decision to announce a buyback alongside its strongest quarterly margin improvement in years reflects confidence that the offshore production ramp-up and backlog conversion trajectory will sustain financial performance improvement through the year.

The Energy Security Tailwind and Its Policy Implications for Wind Orders

The Iran war's disruption of global energy supplies and the resulting elevation of energy security concerns across government and corporate purchasing decisions has created a specific tailwind for wind energy investment that Andersen explicitly referenced in his results statement. Countries that have been reminded by the Hormuz closure of their dependence on fossil fuel imports whose supply can be disrupted by geopolitical events are accelerating their renewable energy deployment programmes in ways that directly benefit wind turbine manufacturers with the production capacity and technology to deliver large projects quickly. The political case for wind energy investment has rarely been stronger than in a period when oil above $100 a barrel is simultaneously straining household budgets, government finances, and corporate cost structures across every energy-importing nation.

European energy policy has been particularly responsive to the energy security imperative, with governments across the continent accelerating their renewable energy deployment targets and streamlining permitting processes to bring wind projects to operation faster than previous regulatory frameworks allowed. The European Commission's REPowerEU programme, initially designed to reduce Russian gas dependence following the 2022 invasion of Ukraine, has been reinforced by the Iran war's demonstration that fossil fuel supply vulnerability extends beyond Russian gas to the entire Gulf energy supply chain that European refineries and power systems depend on. Vestas, as Europe's largest wind turbine manufacturer, is the primary beneficiary of the European policy acceleration, with its order intake and backlog reflecting the commercial consequence of governments urgently seeking to expand renewable generating capacity.

The global energy transition's acceleration in the Iran war environment extends Vestas's addressable market opportunity beyond Europe into Asia-Pacific markets including Australia, Japan, South Korea, and Taiwan, all of which are major fossil fuel importers whose energy security exposure the Hormuz closure has made uncomfortably visible. These markets have been increasing their offshore wind investment programmes as energy security motivations reinforce the climate and cost competitiveness rationales that were already driving renewable energy deployment, and their project development pipelines are creating the order opportunities that will sustain Vestas's intake momentum beyond the current quarter. The combination of European policy acceleration, Asia-Pacific energy security investment, and the ongoing energy transition in developing markets creates the order environment in which Vestas's 20 to 22 billion euro full-year sales guidance is achievable despite the U.S. policy and tariff headwinds that the company has specifically flagged as uncertainty factors.